The European Union is attempting to decouple its artificial intelligence ambition from total reliance on US and Chinese hardware through the creation of AI Factories and the expansion of EuroHPC capacity.

From the Brussels Effect to Industrial Policy

The 2026 Tech Sovereignty Package shifts the Union’s digital posture. For a decade, Europe relied on the “Brussels Effect”—the ability to set global standards through regulation, such as the GDPR and the AI Act. The Commission has recognized that regulation without capacity is a hollow sovereignty. The new framework targets the physical layer: the chips, the power, and the compute required to train frontier models.

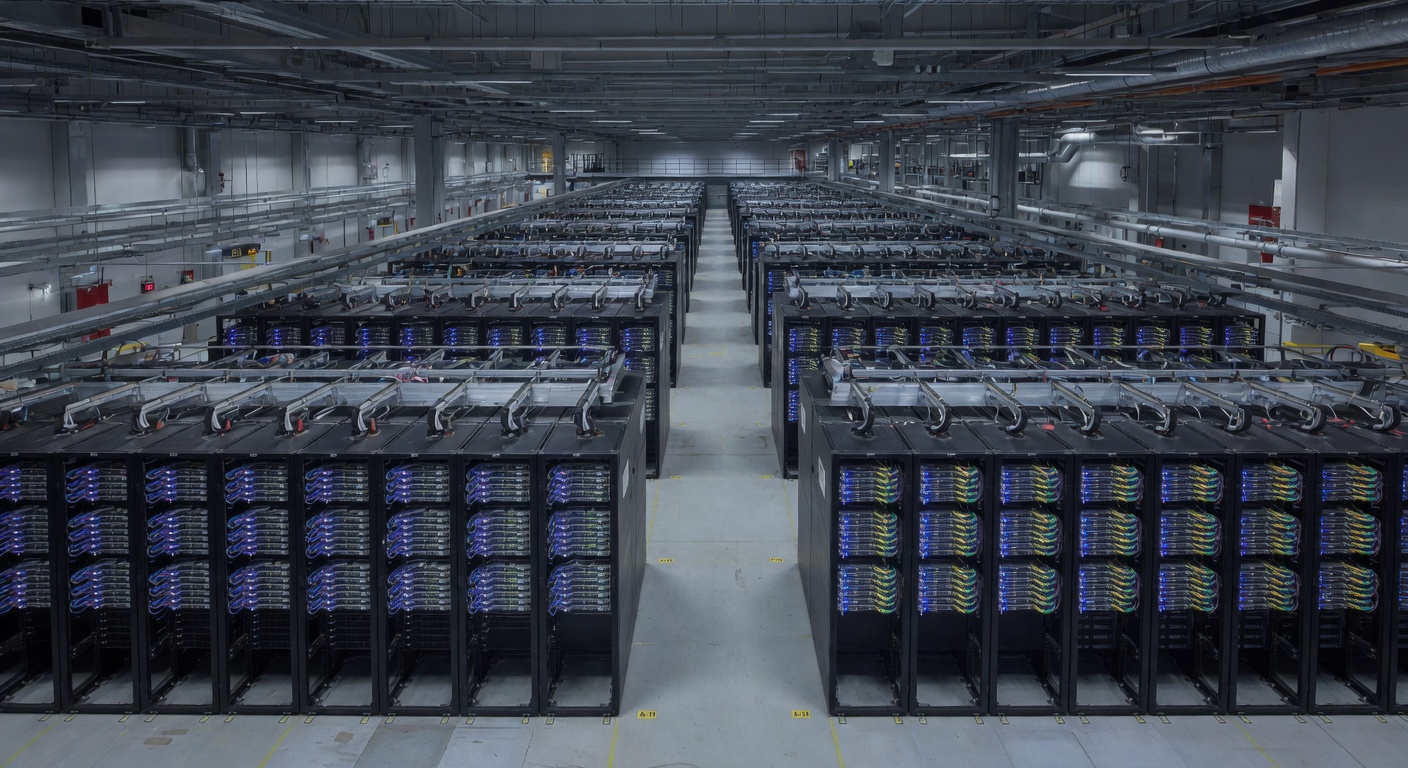

The EU is bridging the “compute gap” by deploying AI Factories—ecosystems that leverage EuroHPC supercomputing power to develop trustworthy generative AI. With 19 factories and 13 “antennas” already operational, the EU is procuring nine additional AI-optimised supercomputers, tripling its current capacity through a €10 billion investment.

This industrial pivot is codified in the Chips Act 2.0 and the Cloud and AI Development Act (CADA). While the AI Act, which becomes fully enforceable in August 2026, focuses on prohibition and risk mitigation, the Tech Sovereignty Package focuses on construction. The most critical bottleneck for European AI is not the law, but the hardware.

The Architecture of Open Strategic Autonomy

The Tech Sovereignty Package converges industrial and legislative tools to operationalize “open strategic autonomy.” Central to this is the Cloud and AI Development Act (CADA), which introduces a four-level certification scheme for cloud and AI services. This framework allows the EU to identify and replace services vulnerable to foreign interference, particularly within the public sector. Parallel to this, the Chips Act 2.0 and the broader EU open-source strategy treat open-source software as a strategic asset rather than a cost-saving measure.

The European Competitiveness Fund supports this shift, providing a centralized mechanism to de-risk deep-tech investments and prevent the relocation of European startups to the US. The strategy draws from the 2024 Draghi competitiveness report, moving the Union toward a model where the state actively shapes the market. The regulatory architecture is now aligned with industrial ambition. The capacity to execute it remains the variable.

The Transatlantic Friction

The transition from regulation to industrial policy has created a diplomatic rift with the United States. US trade groups, including the Information Technology Industry Council (ITIC), argue that the CADA certification and the use of “geographic and nationality-based criteria” are veiled forms of protectionism designed to displace American providers. From the US perspective, the package challenges the dominance of the hyperscalers that underpin the European digital economy.

Within the EU, responses vary between pragmatic cooperation and deeper suspicion. While EU ambassadors have joined “Pax Silica,” a US-led club for securing AI supply chains, some MEPs argue that the US should be viewed with the same scrutiny as China due to the weaponization of digital dependencies. Commissioner Henna Virkkunen maintains that technological sovereignty is a necessity for fair competition. The diplomacy is a paradox. Europe is attempting to build a wall using the bricks provided by its allies.

The Industrial Viability Gap

The ambition to build “AI Gigafactories”—facilities capable of training trillion-parameter models with over 100,000 advanced processors—faces a harsh market reality. While the InvestAI Facility provides €20 billion in funding, some companies bidding for these projects are threatening to pull out. This pattern suggests a lack of genuine industrial appetite or a failure of the European ecosystem to produce the talent and demand necessary to sustain such scale.

A structural conflict also exists between this industrial drive and the AI Act, which becomes fully enforceable in August 2026. Federally funded AI Factories may produce models that are subsequently banned or deemed non-compliant under the Act’s strict human rights mandates. As EDRi notes, the AI Act’s failure to set a “gold standard” for human rights leaves loopholes that clash with the goal of “trustworthy” AI. The EU is building the hardware for a market that its own laws may restrict. The value capture continues to flow upstream to US providers.

The Infrastructure Paradox

The shift toward a capacity-building strategy admits that the “Brussels Effect” is insufficient when the underlying hardware is foreign. By investing in AI Factories and Gigafactories, the EU is attempting to build an industrial base that can sustain its regulatory ambitions. This creates a structural tension: the Union is scaling compute capacity while simultaneously tightening the legal constraints on how that compute can be used. Whether this industrial push can outpace the bureaucratic friction of the AI Act is the critical variable.

The hardware is arriving. The legal certainty is not.

Sources

- digital-strategy.ec.europa.eu

- Deep dive into the structural hardware constraints and the “compute gap” thesis.

- Analysis of the geopolitical friction and US-EU diplomatic tensions.

- Direct policy details on the implementation of AI Factories.

- Digital rights perspective on the package’s goals.

- Counter-perspective on the tension between industrial scale and human rights.

- Timeline for high-risk system bans, providing the enforcement context.

- Market reality check to ground the industrial claims.